Elektronická Evidence Tržeb 2.0 (EET 2.0) is the Czech Republic’s new electronic sales recording mandate. It applies to businesses that accept qualifying in-person payments in the Czech Republic – including international POS software providers and global retailers with Czech operations. The planned go-live date is 1 January 2027. The law is currently a bill before parliament. The final text may change before enactment.

What Is EET 2.0?

EET 2.0 is the second generation of the Czech Republic’s electronic sales recording system, proposed under the draft Sales Registration Act. The Czech Financial Administration (Finanční správa) oversees the system.

The original EET system ran from 2016 and was abolished in 2022. The government concluded that the tax compliance benefits did not justify the complexity it imposed on businesses. EET 2.0 reflects a revised calculation: the authorities believe significant tax revenue is still going unreported, and a modernised system is needed to close that gap.

EET 2.0 is designed to be simpler than its predecessor. It operates in a single online-only mode and requires a leaner data set per transaction. There is no mandatory receipt printing. Inspectors also lose the power to close business premises – a key change from the original regime.

The core mechanic is straightforward: when a qualifying payment is made, the business transmits a summary of that transaction to the Czech Financial Administration in real time. EET 2.0 sits within a broader European trend toward continuous transaction controls, of which the EU ViDA directive is the EU-level framework. EET 2.0 is a sovereign Czech decision – it is not mandated by ViDA.

Who Must Comply – and Who Is Excluded

EET 2.0 applies to personal income taxpayers and corporate income taxpayers who receive qualifying sales in the territory of the Czech Republic. This includes businesses of all sizes that accept contact payments at the point of sale – cash, card, QR code, and cryptocurrency payments made during in-person contact with the customer or at the business’s establishment.

Remote payments – those made without direct physical contact between seller and customer – fall outside the scope of EET 2.0.

Several sectors and transaction types are excluded from the mandate. The draft law identifies financial institutions, public sector entities, transport services, school catering, vending machines, and pre-Christmas carp sellers as excluded. Taxpayers with annual income at or below CZK 1 million may opt for the EET OFF regime instead: a flat monthly payment of CZK 1,500 in lieu of per-transaction recording.

The full statutory exclusion list will be confirmed when parliament passes the law. Businesses that are not clearly excluded should plan for compliance.

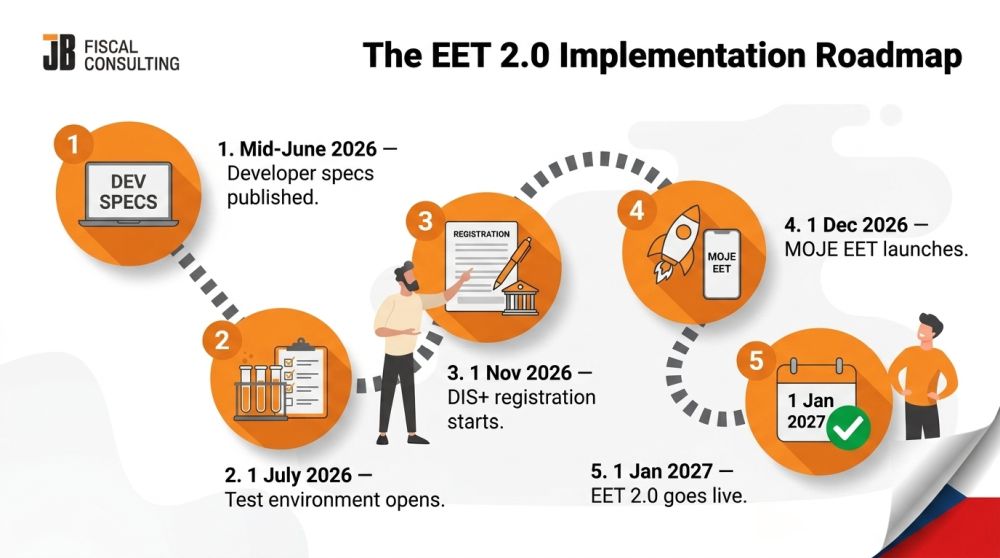

Key Dates – The EET 2.0 Implementation Roadmap

The Czech Financial Administration has set out a phased roadmap toward the 1 January 2027 go-live. Note that the law has not yet passed parliament, and the timeline remains subject to change. With that caveat, the milestones businesses and developers should track are:

1. Mid-June 2026 – As announced, technical specification for developers has just been published by the Financial Administration.

2. 1 July 2026 – Test environment opens for developer integration testing.

3. 1 November 2026 – EET 2.0 registration functions go live in the DIS+ portal. Businesses can begin registering sales units and generating certificates.

4. 1 December 2026 – MOJE EET, a free government web application intended for the smallest taxpayers, is planned to launch.

5. 1 January 2027 – System go-live, with a trial period before full enforcement begins.

How to Register – DIS+ and the CA EET Certificate

Every sales registration unit must be reported to the authorities before it can record sales. Businesses do this through the DIS+ portal on mojedane.cz, the Czech ‘My Taxes’ platform.

Every transaction submission under EET 2.0 must be signed with a digital certificate. This certificate confirms the submitter’s identity and guarantees data integrity. The certificate is issued through CA EET, the dedicated certificate authority for the system.

VAT and Tax Changes Bundled into EET 2.0

EET 2.0 arrives with several tax changes that directly affect POS software configuration, particularly for the HoReCa sector (hotels, restaurants, and cafes).

First, the VAT rate on non-alcoholic beverages served in hospitality settings drops to 12%. POS systems operating in restaurants, cafes, and hotels will need to apply separate VAT treatment to alcoholic and non-alcoholic drinks. This is a configuration change that requires advance testing.

Second, tips received by hospitality staff become exempt from income tax and social security contributions. POS systems that record gratuities will need to separate them from taxable turnover.

What Is Still Unknown

EET 2.0 is a draft law. Several operational questions remain open, and businesses should monitor developments closely.

Penalties: The draft removes the power to close business premises, but the penalty structure for specific violations is not yet fully defined. The bill currently states a general fine of up to CZK 500,000. More precise figures for specific cases of non-compliance have not been published.

Technical specification: Although the technical specification has recently been published-allowing POS software developers to begin development-the absence of the final legal wording means that not all details are fully clarified, and therefore full software compliance cannot yet be guaranteed.

The bill also leaves a number of edge-case scenarios without definitive guidance. JB Fiscal Consulting’s Regulatory Monitoring service tracks Czech law developments and notifies subscribers as soon as material updates are published.

Frequently Asked Questions

Is EET 2.0 already in force?

No. As of May 2026, the Czech government approved the draft Sales Registration Act on 6 May 2026 and forwarded it to parliament. The law is not yet enacted. The current go-live target is 1 January 2027, with a trial period before full enforcement. The final text may be amended before the law passes.

Do we need to replace our existing cash registers?

Not necessarily. EET 2.0 allows businesses to use existing devices – mobile phones, tablets, laptops, or existing cash registers – provided they are updated to support the new system. Businesses should contact their solution provider to confirm EET 2.0 readiness. The Financial Administration also plans to provide a free web application (MOJE EET) for the smallest taxpayers with simple workflows.

Does EET 2.0 cover online payments?

EET 2.0 covers contact payments – those made during direct in-person contact with the customer, or at the business’s physical establishment. This includes cash, card, QR code, and other common methods of payment on-site. Payments made remotely, without direct physical contact, are excluded. For multichannel retail scenarios, JB Fiscal Consulting recommends seeking specific guidance for your architecture.

We are an international company with operations in the Czech Republic. Does EET 2.0 apply to us?

The draft law applies to personal income taxpayers and corporate income taxpayers who make qualifying sales in the territory of the Czech Republic. If your business generates qualifying sales in the Czech Republic, EET 2.0 is likely to apply regardless of where the company is registered. JB Fiscal Consulting recommends seeking specific advice for cross-border structures before the law is enacted.

How does EET 2.0 relate to Czech e-invoicing?

Fiscal receipts and e-invoices are separate legal instruments governed by different laws.

Specifically, fiscalization rules will cover transactions based on payment type, not customer type.

On the other hand, currently there is no mandate requiring businesses to issue e-invoices in B2B transactions, although it is possible and subject to mutual agreement.

What is left to be defined in the near future is coexistence of the fiscalization obligation and the optional e-invoicing procedure and whether there are overlapping consequences. However, it is necessary to keep in mind that fiscalization is focused on reporting sales to the authorities while e-invoicing, as it exists today in Czech Republic, is focused on the invoice exchange itself, between the parties involved.

Next Steps

EET 2.0 is still developing. Besides the need to detailly analyze the technical specification, final exclusions list, and confirmed penalty structure are all pending. If you need to track Czech law changes as they happen, JB Fiscal Consulting’s Regulatory Monitoring service covers the Czech Republic as part of its 45+ country portfolio. For questions specific to your POS architecture or compliance scope, book an Essentials Session or Consulting Session with our senior consultants.

The information on this page does not constitute legal advice. JB Fiscal Consulting cannot be held responsible for errors or omissions. Please contact us if you have specific questions about your compliance situation.